Unsurprisingly, the Canada Revenue Agency (“CRA”) followed the Internal Revenue Service (“IRS”) in seeking a court order for records from cryptocurrency exchanges. The tax authorities prevailed in both cases, increasing the transparency of cryptocurrency trading and investing.

Especially in its earlier days, cryptocurrency had a reputation as an underground currency providing secrecy and facilitating black-market transactions. This notoriety began to recede when in November 2016 the IRS (the US tax authority) filed a generic request, known as a “John Doe” summons, on all U.S. Coinbase customers who had transferred Bitcoin between 2013 and 2015. The IRS initially sought all records, including third party information.

While the US District Court – California Northern District (San Francisco) (Case 3:17-cv-01431-JSC) found that the IRS request was broader than necessary, it nonetheless ordered significant disclosure from accounts having a minimum of $20,000 in any one transaction during the 2013 to 2015 time period. The disclosure included the taxpayer’s identification number, name, birthdate, address, records of account activity, and all periodic statements of account.

Accountants, engineers, lawyers, doctors, dentists. Now real estate professionals join the Ontario regulated professionals who are able to personally incorporate their business. Following several other provinces,[1] on October 1 2020, the Ontario government passed O/Reg 536/20: Personal Real Estate Corporations, under the Real Estate and Business Brokers Act, 2002, which provides that real estate salespeople and brokers may incorporate in Ontario. Incorporation allows a real estate professional to have their self-employed revenue paid directly into their personal real estate corporation (“PREC”), offering some tax advantages.

Tax Advantage

The key tax advantage of incorporation is that income earned in a PREC is taxed at the corporate tax rate, which is substantially lower than the personal tax rate.

In Ontario the combined federal and provincial corporate tax rate is 12.5% on the first $500,000 of active business income (a threshold amount that is shared among associated corporations), and 26.5% on income above that threshold. In contrast, the highest personal tax rate is 53.52% on income over $220,000. As a result, when income is retained in a PREC and taxed at the corporate rate, a greater amount of money is available for investment.

For example, if a real estate professional earned $500,000 in a year, without a corporation the professional would have approximately $266,344 of after tax income that could be invested. In contrast, making use of a PREC, the same income would result in approximately $437,500 of funds available for investment within the corporation.

This may increase the investment growth and allow an investment portfolio or a retirement portfolio to grow more quickly, keeping in mind that within the corporation the investment income itself will likely be taxed a higher rate than the active business income.

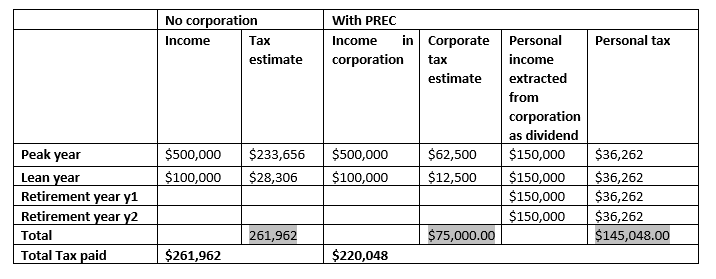

An additional tax advantage is that the real estate professional can distribute their career earnings over their lifetime. Rather than pay the highest personal tax rate in peak earning years, the real estate professional can extract income from the corporation in leaner years, or in retirement, at a lower marginal tax rate. For example:

As the chart indicates, using a PREC allows a real estate professional to distribute income earned over multiple years, in turn allowing the professional to access lower marginal tax rates. This can reduce the total amount of taxes paid over a lifetime.

Life Insurance

A further benefit offered by a PREC is that life insurance for the controlling shareholder can be held within the corporation, reducing the amount of pre-tax earnings required to cover the premiums. In addition, life insurance benefits, less the adjusted cost base of the policy, are credited to a corporation’s capital dividend account (“CDA”) and can be extracted from a corporation free of tax. The reduction of the credit to the CDA by the policy’s adjusted cost base is intended to offset the advantage of paying insurance premiums with corporate income, instead of personal income taxed a personal tax rates. Real estate professionals considering having a PREC purchase life insurance should also note that in most cases the PREC will not be entitled to deduct the expense of the insurance premiums.

Income Splitting

The 2017 amendments to the Income Tax Act introduced the tax on split income rules, know as “TOSI”, which have significantly curtailed the ability of professionals to use professional corporations to split their income with low earning family members. Previously, professionals could pay dividends from their corporations to family members with low income, allowing the family to benefit from the lower tax rate applicable to the professional’s spouse or children. The TOSI rules now require that in order for corporate dividends to be taxed in the hands of a lower earning family member, that family member must be actively engaged in the professional’s business, meaning, for example, that the family member works in the business at least an average of twenty hours per week.

Restrictions

A PREC can limit a controlling shareholder from standard corporate financial liabilities. However, a PREC does not limit professional liability, which is governed by the Real Estate Council of Ontario pursuant to the Real Estate and Business Brokers Act, 2002.

In addition, like other professional corporations, PRECs are subject to restrictions. In particular, all of the equity shares of a PREC must be held directly or indirectly by the controlling shareholder, being an individual salesperson or broker registered with the Real Estate Council of Ontario;[2] the controlling shareholder must be employed by a brokerage; the controlling shareholder, must be the sole director and officer of the corporation;[3] and family members of the registrant can only hold non-voting and non-equity shares of the corporation.

Conclusion

Given the current “heat” of the Toronto real estate market, incorporation may be an attractive option for real estate agents or brokers. However, unless a real estate professional is earning substantially more than their everyday expenses, incorporation may not be beneficial. Additionally, real estate professionals should take the TOSI rules into account when deciding whether or not to incorporate. Anyone considering establishing a PREC should consult with their tax professionals for specific advice.

[1] British Columbia 2008 – Real Estate Services Regulation – Real Estate Services Act

Saskatchewan – see, Section 5 The Professional Corporations Regulations, 2002 under the Professional Corporations Act.

Quebec see section 34.1 of Regulation respecting brokerage requirements, professional conduct of brokers and advertising under the Real Estate Brokerage Act.

The COVID-19 pandemic has revealed the fault lines of the globalized economy and triggered a rise of protectionist trade policies. The latest chapter in this trend away from a multilateralism is the U.S. withdrawal from OECD negotiations over the tax challenges of the digitalisation of the economy, which in turn has provoked European nations to retreat to unilateral solutions.

The Globalized Economy and COVID-19

In the period between the end of the Second World War and the on-set of the COVID-19 pandemic, the globalization of production created deep economic interdependencies, binding domestic economies to a global supply chain. Consequently, when the COVID-19 pandemic broke, the structure of global trade was such that a disruption in one link of the supply chain created effects all down the line.

In March 2020, the six nations hit hardest by COVID-19 were the U.S., China, Korea, Italy, Japan, and Germany. At the time, these six nations accounted for 55 percent of world supply and demand, 60 percent of world manufacturing and 50 percent of world manufacturing exports.[1] China, where the virus first emerged, was largest contributor to global trade, the “workshop of the world,” making up 41 percent of world manufacturing exports and 20 percent of global trade in manufacturing intermediate products.[2] Due to the globalization of production, when the pandemic decreased production in these six nations, and China in particular, the effects reverberated globally.

In January 2020, the OECD/G20 Inclusive Framework on BEPS, a group of 137 countries including Canada, endorsed a statement, which affirmed their commitment to build a global solution to the tax challenges created by the digitalisation of the economy. This work has been underway since 2015 and is slated to be finalized by the end of 2020.

The statement, itself a political expression of on-going commitment, was accompanied by additional documents which, provide an outline of the “architecture” of the currently agreed upon Unified Approach under Pillar One, a programme of work descriptions, details on the multinational enterprises (“MNEs”) that will be impacted by the initiatives under Pillar One, and a progress report on Pillar Two work (collectively the “January 2020 Statement”). The biggest development presented in this set of documents is the architecture of the Pillar One solution, including a clarified explanation of a new taxing right for market jurisdictions.

On April 22, 2020, the Canada Revenue

Agency (“CRA”) indicated that it would allow special favorable tax treatment to

employees working from home during the COVID-19 crisis.[1]

In particular, the CRA will accept that

the reimbursement of an employee, for amounts spent on personal computer

equipment to enable the employee to work from home, mainly benefits the

employer. As a result, the reimbursed amount will not be a taxable benefit to

the employee. This relief is to apply

for amounts up to $500 and only in respect of amounts for which the employee

provides receipts.

In the normal course, an employer can

provide an employee with an allowance for home office expenses, which is a

taxable benefit for the employee.[2] Alternatively, the employer can decide to

reimburse an employee expense upon presentation of an invoice, in which case

the reimbursement will be a taxable benefit if it primarily benefits the

employee rather than the employer.[3] Usually if an employee receives a

reimbursement for home office equipment, it is characterized as a personal

expense, primarily for the employee’s benefit, and therefore a taxable benefit.

The CRA’s announcement does not change

the tax consequences for employers. An

employer providing an employee with reimbursements for home office expenses,

even certain capital expenses such as the acquisition of tools, will normally

be entitled to deduct the full amount of the reimbursements as a business

expense, provided the amount is reasonable in the circumstances.[4]

[2] See CRA Interpretation, 2011-0402581I7 —

Allowance for workspace in the home, July 12, 2011. See also, CRA,

Interpretation Bulletin, IT-352R2 — Employee’s Expenses, Including Work Space

in Home Expenses, August 26, 1994.

[3] See CRA, Tech Interp, 1999-0013955 —

Construction and expenses — workspace, February 3, 2000.